In the mid-1980s, a tax law was changed that affected every collector in the United States. Previously, when collectors experienced the loss of a single object or collection, they could write off the current appreciated value of the item(s) on their taxes. The new law, however, stipulated that the loss could only be considered at its original acquisition price. This was shocking news for owners of priceless pieces, collections acquired decades before, or objects passed down through generations. With this change, the need for adequate coverage, whether an addendum to a collector’s homeowner’s insurance or a specialized policy, has become necessary. Only then can appreciated value be properly accounted for.

More than Just Bragging Rights

What’s It Worth?

The key to properly insuring a collection of fine art, antiques, or other valuable articles is to know exactly what you have and what it’s worth prior to a loss. Though this may seem straightforward, it is the best way to assure that your insurance will provide you with the proper coverage. The way to ascertain this information is to have a reputable dealer or certified appraiser establish the value of the items in your collection. By doing so, you are prequalifying what you will receive from your insurance policy should a loss occur. Establishing what an item is actually worth after it is lost or destroyed can be a daunting task, and will most assuredly lead to disappointment. Once values have been properly established, you will be able to make an informed decision when selecting insurance. The three most common ways that collectors insure their personal collections are: 1. Under the “Unscheduled Personal Property” section of the homeowner’s policy; 2. Scheduled “All Risk” coverage; 3. Blanket “All Risk” coverage.

Is Your Collection

Worth Half Your Home?——

1. Unscheduled Personal Property

Unscheduled personal property coverage is automatically provided by a homeowner’s insurance policy. In many cases, this coverage will be all that you need to insure your collection. Most homeowner’s policies include coverage for unscheduled personal property that is valued at 50 percent of the amount for which the dwelling is insured. For example, if the house is insured for $200,000, then the unscheduled personal property, or content of the house, is usually insured for $100,000.

Homeowner’s policies, however, vary tremendously by company and each company offers a variety of policies, some broader than others. It is essential that you inform your insurance agent or broker about your collection and its value so that he or she can determine whether your current policy affords you sufficient coverage for your possessions.

Most major insurance carriers provide coverage for contents under their “Deluxe” homeowner’s policies, called all risk insurance (this differs from scheduled all risk insurance, which is separate coverage). This is the type of additional coverage you may need for your collection. Three of the best policies currently available are Chubb’s “Deluxe Masterpiece” homeowner’s policy, Fireman’s Fund “Prestige Plus” homeowner’s policy, and AIG’s Homeowner’s Policy from its Private Client Group. All three provide exceptionally broad coverage for the home and its contents.

A word of caution: Relying solely on homeowner’s coverage for collections has several disadvantages. In the event of a claim, for instance, you have to establish the value of the lost or damaged items to the insurance company. Because many homeowners are not made aware of the need to have their collection appraised, they then have the daunting task of determining values after a loss, which can be quite difficult. In addition, most homeowner’s policies have valuation sublimits for items such as silverware, stamps, coins, gold, jewelry, and guns. These sublimits can greatly restrict what the insurance policy covers.

Another disadvantage is that the property deductible from a homeowner’s policy—which can range from $250 to $25,000 depending on the company and policy—applies to any loss and can negate any compensation if a loss falls within that threshold. Finally, breakage of fragile items made of glass, ceramics, and marble is not covered under many homeowner’s policies.

Peace of Mind——

|

|

|

|

|

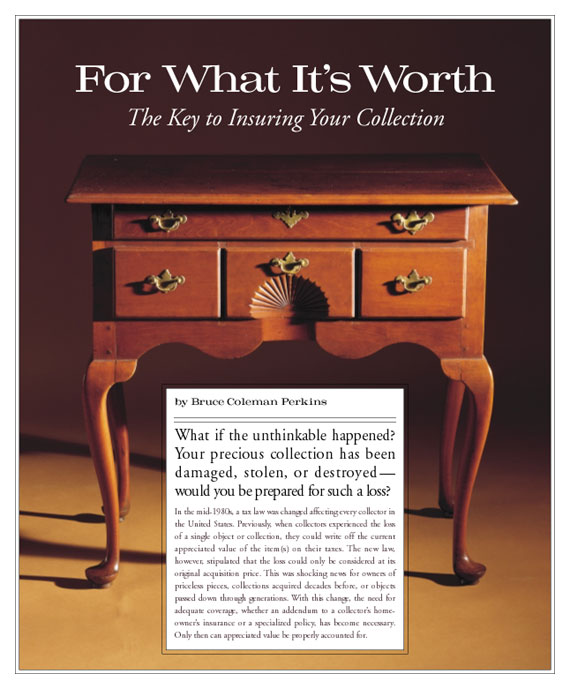

Art and antiques often increase in value over time. The Queen Anne cherry dressing table (top) from Wethersfield, CT, ca. 1750–1770, illustrates the importance of having a collection properly insured for replacement in the event of a loss. In 1980, dressing tables of similar form and design would have sold for $30,000 to $50,000 and in today’s market they can bring $70,000 to $100,000.1 Likewise, prices for fine paintings are also on the rise. Guy Wiggins’s (American, 1883–1962) At the Plaza, ca. 1940, (above) has had a sixfold increase in market value in the last ten years, with a current valuation of $140,000. Courtesy of Vose Galleries of Boston. |

2. Scheduled “All Risk” Coverage

For most people, the best approach to properly insuring a collection is to use a scheduled all risk policy—also known as a “Fine Arts” or “Valuable Articles Policy”—in addition to regular homeowner’s insurance. With this type of policy, each item is individually listed at a predetermined or “agreed” amount and is provided the broadest available coverage (including breakage). There is no deductible amount that applies and coverage is provided on a worldwide basis if collections should be transported. There is also automatic

coverage for new acquisitions (with certain restrictions).

With this coverage, losses are prequalified. If an item is stolen, damaged, or destroyed, the insurance company will pay the claim based on the predetermined amount. In most cases, for peace of mind, this is the best type of coverage.

The only disadvantage to this policy is that over time the market value of some of the scheduled items will increase and may exceed the amount for which they are insured. This concept was driven home when my son’s errant toss of a baseball took out an eighteenth-century English wine glass. The glass was covered, to be sure, but its present value was three times my original purchase price. Although I was compensated for the glass, I could not replace it. This type of scenario can be easily rectified if the values of your objects are updated periodically, generally every five years. Additionally, several insurance companies, such as Chubb and Fireman’s Fund, have added an endorsement to their polices to provide coverage of up to 150 percent of the scheduled amount if the actual replacement cost increases beyond the predetermined amount.

This Is the Limit——

3. Blanket “All Risk” Coverage

The third option is Blanket “All Risk” coverage. This insurance is written according to a total dollar valuation and does not require items to be individually listed. As with the scheduled all risk policy, a deductible amount does not normally apply, coverage is written on a worldwide basis, and there is coverage for breakage of fragile items.

Although this coverage provides more flexibility to the insured before a loss, it places a greater burden on the policyholder to have all items properly appraised and documented before anything happens to them. By so doing, a benchmark for future evaluation is established that will simplify determining current market values if needed.

Please be aware that most of these blanket policies are written with a per item limit. Traditionally that limit has been $2,500 per item; however, most of the better carriers are willing to increase that amount to meet the client’s needs. The answer for some collectors is a blended policy that combines scheduled coverage for more valuable items and blanket coverage for items under the $2,500 threshold.

You Don’t Buy a Porsche

from a Chevy Dealer

Like collecting, insuring your items is very subjective. As a

collector, you put a great deal of time and effort into selecting what you will buy and from whom you will buy it. The same should hold true when insuring your valuables. It stands to reason that you should use an insurance agent or broker who is well versed in covering fine art and antiques and who will assist you in selecting the type of policy that best suits your needs. Ask a lot of questions. If your agent cannot answer your queries

satisfactorily, then check with your fellow collectors or with dealers you trust for the name of a broker who can provide you with coverage that will protect your investment and give you that most precious of commodities—peace of mind.

Options for Insuring Your Collection

Unscheduled Personal Property

section of the homeowner’s policy

• Covers up to 50 percent of the value

of the dwelling

• Policies differ tremendously by company

• Difficult to determine value “after the fact”

• Sublimits may restrict what the policy covers

Scheduled “All Risk” coverage

• Also known as a Fine Arts or Valuable

Articles policy

• Each item listed individually

• No deductible

• Breakage coverage for fragile items

• Worldwide coverage

• Automatic coverage for new acquisitions

Blanket “All Risk” coverage

• Written on “total dollar amount”

• No deductible

• Worldwide coverage

• Breakage coverage for fragile items

• Burden of proof of value falls on insured

• Per-item dollar limit

Bruce Coleman Perkins is principal of Flather & Perkins, Inc., in Washington, D.C., an insurance company offering coverage of fine and decorative arts collections for museums, galleries, and private collections. He is on the boards of Winterthur Museum, The Decorative Arts Trust, The Visiting Committee of the Peabody Essex Museum, and is a founding member of the Washington Decorative Arts Forum.

|